- Emma Parker

- March 24, 2026

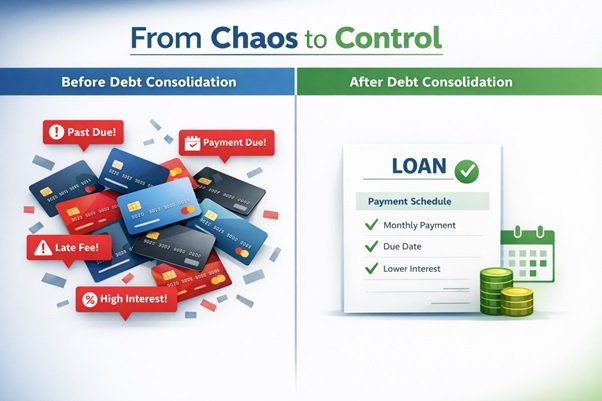

The situation of addressing credit card debt on many accounts is very daunting. The cards will require two different due dates and minimum payments.

The credit cards are consuming your money through the high APR charges. A considerable percentage of every pay is spent on interest, which is usually more than 20%. This puts you in the rat race that is difficult to escape.

Many people initially search for quick cash loans near me when feeling the pressure of mounting debts. These may only alleviate the immediate, but consolidation loans are a more viable long-term solution to the real problem.

How Consolidation Loans Clear Card Debts?

All cards have their payment date, interest rate, and payment minimum. A £1500 debt consolidation loan can simplify your finances and save you money. In case you take a loan for consolidation, you end up repaying all your credit cards at once.

The interest rates on most credit cards are high and variable. The rates of the consolidation loans are usually lower and fixed. This way, you will be sure of the amount that you will be paying every month until the loan is cleared.

Credit cards use compound interest, which means interest builds on interest. This has the potential to increase your debt. With a simple interest, this snowball effect does not exist with consolidation loans. Unlike credit cards, you do not have to get more money every time you make a payment back to your loan balance.

Late payments due to credit card default incur late charges and increased charges. You are less likely to miss a deadline with a single payment of a loan.

Types of Consolidation Loans to Clear £1500 Debt

Finding the right loan matters just as much as deciding to consolidate. Many options are available for borrowers looking to clear small credit card debts of around £1500.

High Street Banks

Most large banks have personal loans which can be used to consolidate them. They often have competitive rates for existing customers. You submit the application in person. Some prefer this because of financial reasons.

Online Lenders

Online lenders often approve loans faster than traditional banks. Small loans from a direct lender with minimal paperwork and quick fund transfers to your account help you a lot in a crunch debt situation. This application process does not require days to be completed, but just a few minutes.

Peer-to-Peer Platforms

P2P lending links the borrowers and the individual investors. These platforms tend to be very competitive in terms of their prices if you have a good credit rating. The application is online, and the money is typically received within days after approval.

Specialist Debt Consolidation Companies

Some companies focus solely on helping people consolidate debts. They can provide available assistance, such as financial advice, with the loan. These experts are aware of the usual issues in debt and can find ways to resolve your predicament. They could also have less rigid requirements than the banks when accepting applications.

| Debt Consolidation Pros vs Cons | |

|---|---|

| Advantages | Disadvantages |

| Single monthly payment | Risk of new debt accumulation |

| Lower interest rates | Longer repayment period possible |

| Fixed payment amount | Monthly payment may increase |

| Improved credit score potential | Loan approval not guaranteed |

| Reduced financial stress | Early repayment fees |

| Clear debt-free date | Temptation to overspend |

| Stop late fees and penalties | May pay more interest long-term |

| Simplified budgeting | Requires financial discipline |

Step-by-Step Debt Clearing Process

With the help of a consolidation loan, it is simple to clear your credit card debts. You can follow the steps to make sure that you get the best offer and use the loan.

- Step 1: Add the names of all your credit cards, their balances and interest rates. You should be sure to record any annual or special conditions or charges per card.

- Step 2: Sum all balances until you end up with the amount you are supposed to borrow. In this case, if your cards add up to about £1500, that’s your target loan amount.

- Step 3: Check your credit score before applying. This will help in creating realistic expectations as regards what rates you will qualify for. There are free tools that allow you to test your score without influencing it.

- Step 4: Research on lending options with different lenders. Compare interest rates and conditions of repayment and other fees.

- Step 5: You should forward your application to the lender with the most favourable terms for your case. Prepare your financial information, such as evidence of income and your current debt situation.

- Step 6: This is because as soon as the money gets approved into your account, you should pay off all your credit cards first.

- Step 7: Another tip is to think about cutting the cards into fragments or locking them up. It is always a good idea to have one in case of an emergency, and eliminate the temptation to let new debt pile up at the expense of settling your loan.

- Step 8: You can have a direct debit for your loan payments. This will guarantee that you do not miss out on payments and protect your credit score in the repayment period.

When Consolidation Isn’t Right?

Very minor debts might not be worth consolidating. The savings on interest might be minimal for short-term debts.

Some credit cards have interest-free stipulations. The consolidation loan with interest will not help you save. In this instance, it is more prudent to focus on repaying it during the interest-free period.

The credit score is a critical factor in the type of loan rate you are charged. You might not qualify for better rates than you currently have if your score has dropped since you got your credit cards. You should perhaps do better to improve your score.

The uncertainty about a change of job is very dangerous for acquiring a new loan. Your credit cards will at least allow you to make minimum payments in tight months.

Debt consolidation is a form of treating a symptom rather than a cause. You are likely to be paying loan payments as well as your new credit card debt unless you change your spending patterns.

- Consider before you decide to use cards once more

- Think about the term of the loan

- Check the early repayment charge

- Balance transfer cards may help in certain cases

- Free debt advice services can help you decide what’s best

Conclusion

Consolidating your credit cards will put you in charge of your credit card issues. You are no longer required to make payments of varying amounts.

A single and constant payment will make you confident enough to plan. This has a definite expiry date for a consolidation loan. One has a definitive finish line to strive to achieve. According to many borrowers, the relief is experienced immediately after their cards have been cleared.

Emma Parker is a financial counsellor at LondonLoansBank and has been serving for over 5 years. She is a psychology graduate from the University of Glasgow. Since she has keen interest in the finance field, she pursued a diploma course in banking and finance that led her to opt for her current career. She assists people choose the best loan based on their current financial situation and credit score. As Emma understands how people react to money problems, she gives them a helping hand to solve their financial complications.

Recent Posts

May 28, 2026

March 20, 2026

March 18, 2026

February 23, 2026

February 18, 2026

January 22, 2026

January 12, 2026

January 10, 2026

December 23, 2025